Founders should focus on lengthening their runway, – which means focusing on maximum growth for minimum cash burn. We are coming back to times when profitability, Free Cash Flow, and positive unit economics matter.

Tooploox is a tech-focused company, yet we consider our role broader than simply delivering code and digital products. We consider ourselves startup and investment advisors, especially considering the venture capital experience of our staff.

This text was delivered by Robert Ditrych, investor and Tooploox Chief Strategy Officer.

One year ago I wrote an article (Public equity: investment tactics for the rest of the Year 2021) where I presented my views on the market and shared investment tactics for the rest of the year 2021. The first and most important conclusion encouraged investors to consider limiting exposure to hyper-growth stocks as a category particularly vulnerable to changes in long-term interest rates:

It is all about discount rates. If you do not want to be highly exposed to inflation risk, you might consider limiting your exposure at the long end of the curve. Hold only your highest conviction positions! – May 3, 2021

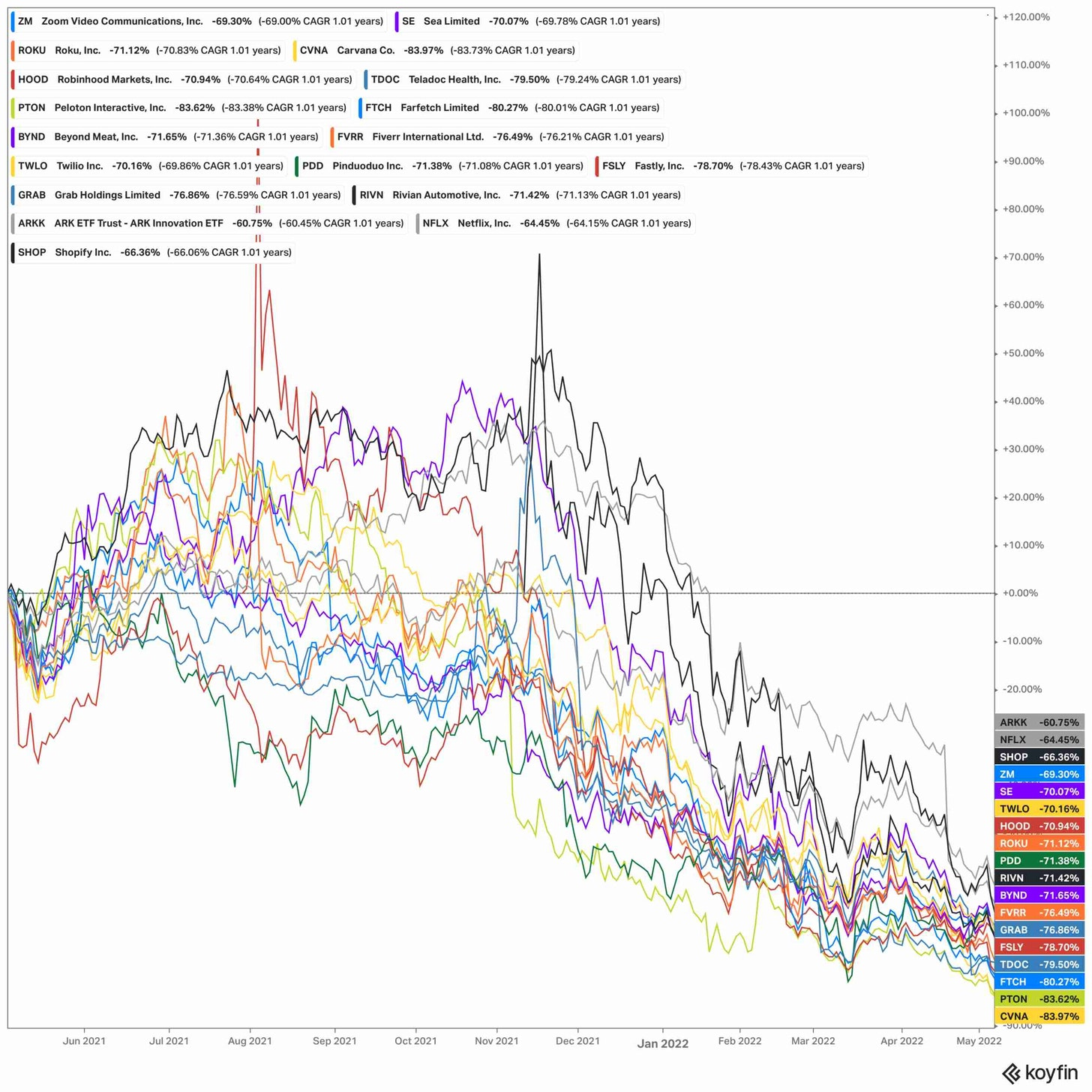

As we’ve found out, that was a timely consideration… not perfect timing, as the market didn’t look so bad till mid-November, but now it has already begun to look pretty nasty. Here is a look at selected hyper-growth representatives’ performance:

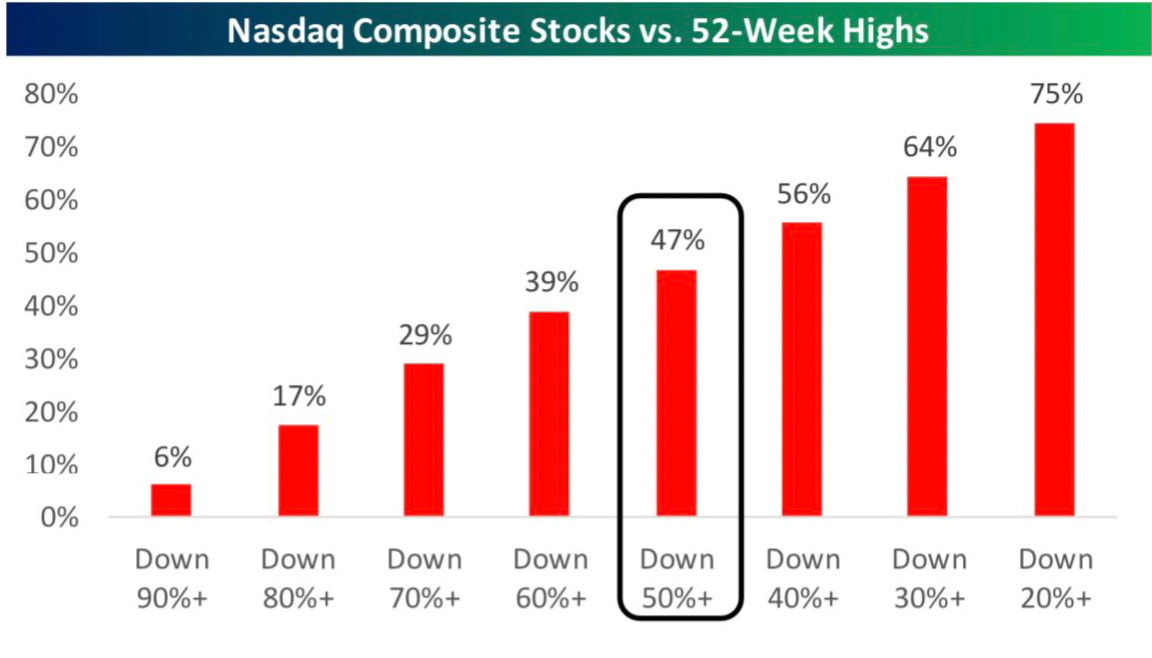

The most respected growth ETF at that time – Cathie Wood’s ARK Innovation ETF Fund – once named as a new Berkshire Hathaway – lost more than 60% of its value, while Covid’s stars, such as Peloton ($PTON), Carvana ($CVNA), and Teladoc Health ($TDOC), lost about 80% of their value. In the same period, Nasdaq lost 7%, while S&P500 gained 2%. Indexes are somehow masking the pain of many stockholders as almost half of Nasdaq’s stocks have been cut in half from a 52-week high and 75% of stocks lost more than 20% in value:

Why is that?

Basically, trillions of dollars of the money printed in response to Covid caused an asset appreciation and a spike in inflation. That turned the Fed towards becoming hawkish with its approach to inflation, which caused interest rate expectations to rise. As a consequence, that change hammered growth stocks.

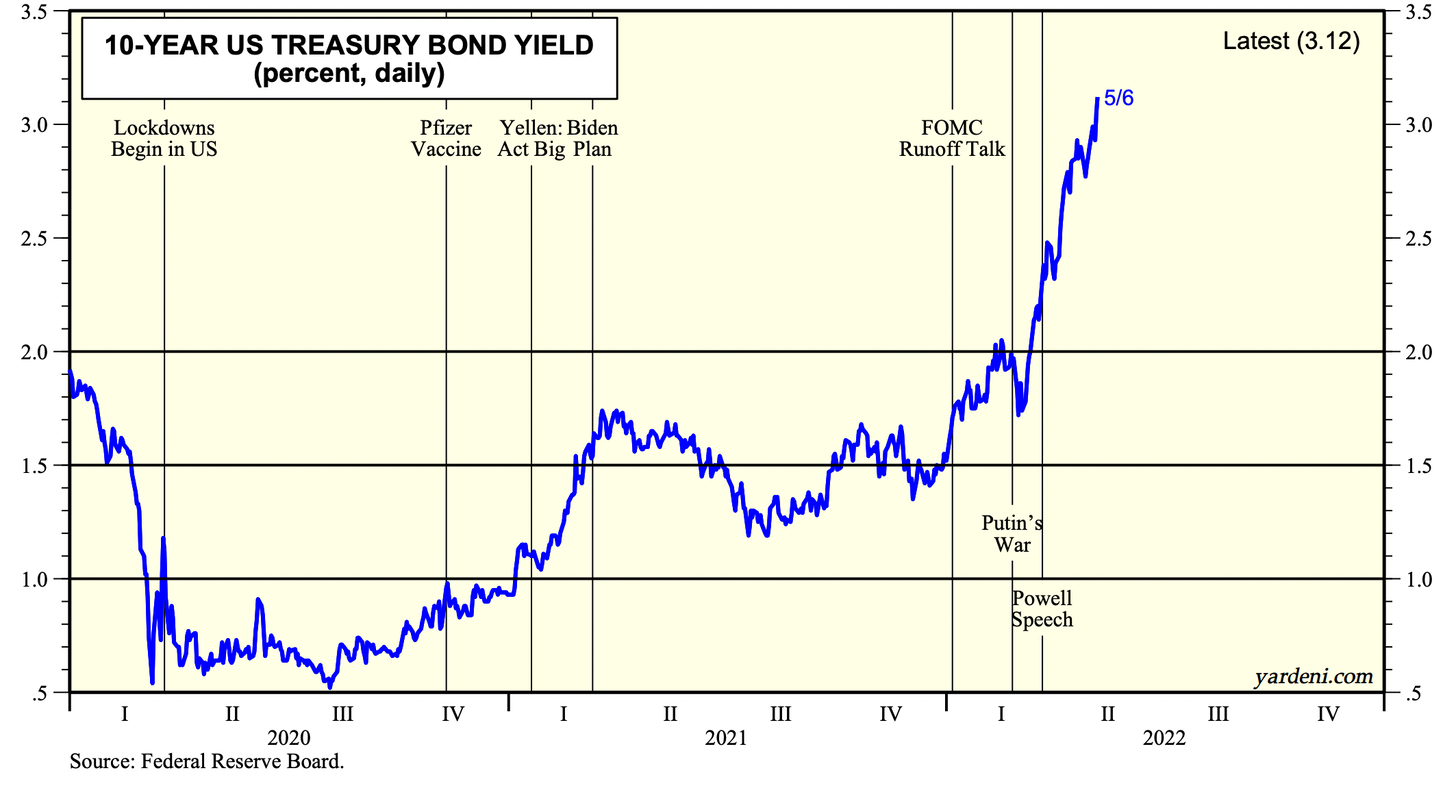

To understand factors that put downward pressure on prices of growth and tech stocks we have to look at changes in the market risk-free rate (Rf). In valuations we used to take long-term (10 or 30-year duration) government bond yields as a proxy of the risk-free rate, which is a component of the discount factor:

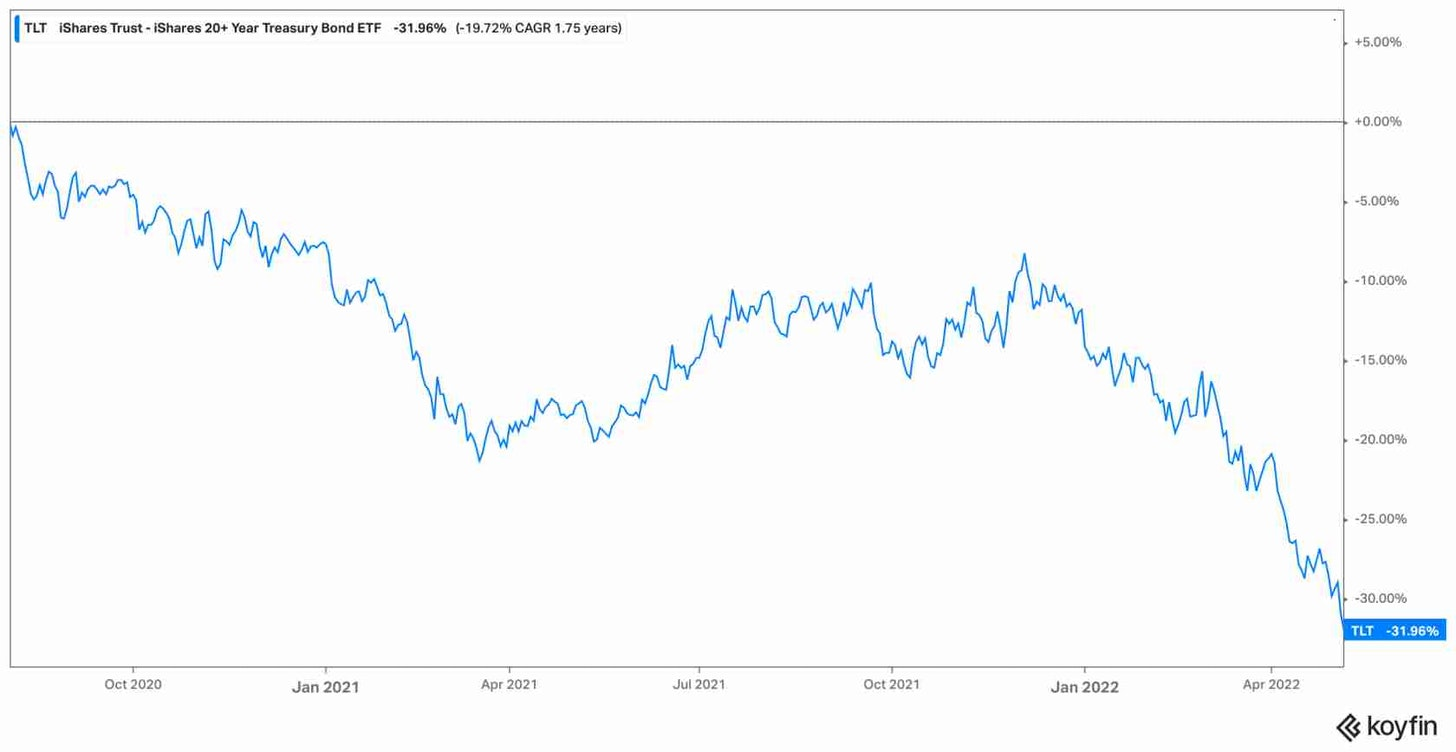

As inflation is raging, bond yields are climbing higher and higher, pushing down the value of discounted cash flows (especially of those far into the future as 10 or 30-year bond principal payments, or terminal value of growth companies and early-stage startups). So far in 2022 bonds have lost 10% – one of the worst returns in US history:

Almost never has the U.S. bond market lost as much money as in the first four months of 2022, according to Edward McQuarrie, an emeritus professor of business at Santa Clara University who studies asset returns over the centuries. – source: WSJ’s article “It’s the Worst Bond Market Since 1842. That’s the Good News.”

ETFs with exposure to Long-term bonds (20+ Years) lost a shocking 32% of value since August 2020 (chart below), and those are the result before inflation. Overall, almost no mixed Bond/Equity strategy has worked in the last couple of quarters as inflationary pressure depreciated the value of future cash flows.

Implications for VCs and startup founders.

As a consequence of the above changes, investor sentiments in Silicon Valley are the most negative since 2001. I recommend you to read David Sacks’ (co-founder of Craft Ventures & former COO of Paypal) thread on Twitter.

Key conclusions:

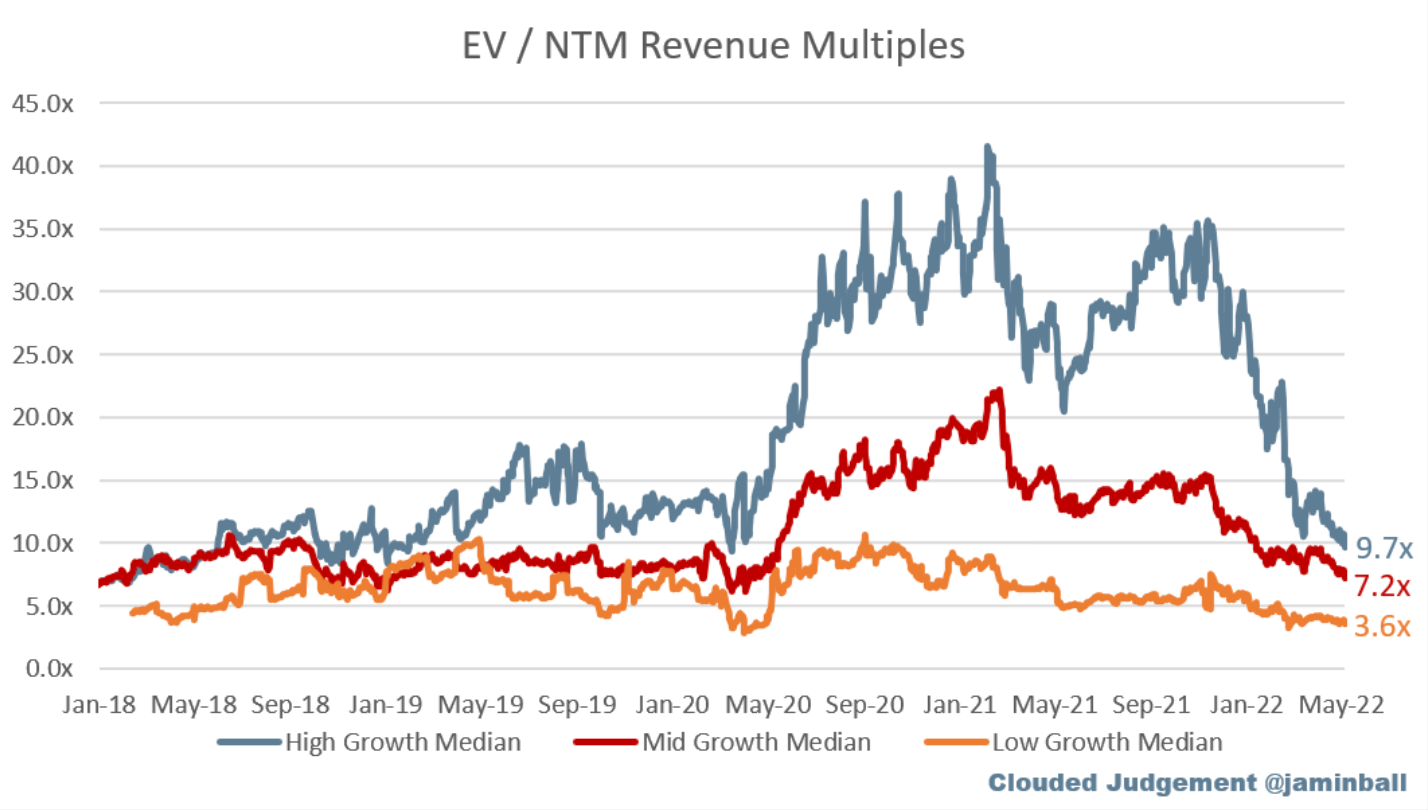

The market valuation multiples reverted to pre-covid means (i.e. covid multiples were a market aberration). Here is an example of Cloud business valuation multiples (EV/Revenue):

- The market will go up or down based on rate expectations and changes in earnings:

- If inflation proves transitory, there is an upside, but the reverse is also true: if inflation proves more persistent, there is a downside.

- There is also a risk to earnings from a slowdown in the economy. This has not broadly materialized yet outside of Covid stocks (eg. Zoom, Peloton, Netflix).

- The abundance of “cheap” VC money seems to be over as the growth stock crash caused a rapid chilling of the VC market. How?

First, private markets derive valuations from public comparables (so private rounds are also going down).

Secondly, large crossover investors (operating both in public & private markets) went into preservation capital mode and liquidity has dried up.

As liquidity has dried up, the most flexible capital is found in leaving the system.

So what should startup founders do?

Founders should focus on lengthening their runway. It means focusing on maximum growth for minimum cash burn. We are back to times when profitability and FCF matter (or at least positive unit economics in the early stages).

I would just like to bring up a note that Sequoia sent (in March 2020) to startup founders to help them navigate potential business consequences of the spreading effects of the coronavirus. Now, it might be a time to draw from their wisdom:

We suggest you question every assumption about your business, including:

- Cash runway. Do you really have as much runway as you think? Could you withstand a few poor quarters if the economy sputters? Have you made contingency plans? Where could you trim expenses without fundamentally hurting the business? Ask these questions now to avoid potentially painful future consequences.

- Fundraising. Private financing could soften significantly, as happened in 2001 and 2009. What would you do if fundraising on attractive terms proves difficult in 2020 and 2021? Could you turn a challenging situation into an opportunity to set yourself up for enduring success? Many of the most iconic companies were forged and shaped during difficult times. We partnered with Cisco shortly after Black Monday in 1987. Google and PayPal soldiered through the aftermath of the dot-com bust. More recently, Airbnb, Square, and Stripe were founded in the midst of the Global Financial Crisis. Constraints focus the mind and provide fertile ground for creativity.

- Sales forecasts. Even if you don’t see any direct or immediate exposure for your company, anticipate that your customers may revise their spending habits. Deals that seemed certain may not close. The key is to not be caught flat-footed.

- Marketing. With softening sales, you might find that your customer lifetime values have declined, in turn suggesting the need to rein in customer acquisition spending to maintain consistent returns on marketing spending. With greater economic and fundraising uncertainty, you might even want to consider raising the bar on ROI for marketing spending.

- Headcount. Given all of the above stress points on your finances, this might be a time to critically evaluate whether you can do more with less and raise productivity.

- Capital spending. Until you have charted a course to financial independence, examine whether your capital spending plans are sensible in a more uncertain environment. Perhaps there is no reason to change plans and, for all you know, changing circumstances may even present opportunities to accelerate. But these are decisions that should be deliberate.

Having weathered every business downturn for nearly fifty years, we’ve learned an important lesson — nobody ever regrets making fast and decisive adjustments to changing circumstances. In downturns, revenue and cash levels always fall faster than expenses. In some ways, business mirrors biology. As Darwin surmised, those who survive “are not the strongest or the most intelligent, but the most adaptable to change.”

A distinctive feature of enduring companies is the way their leaders react to moments like these.

To sum up:

- If you are in a funding cycle as a founder, you should raise your funding as soon as possible & raise as much as possible.

- Focus on fundamentals!

- Stay realistic on valuations.

Innovation will not stop here (as some of the best companies were created during down markets), but the “free money” party is over! Beware that on whatever side (as an investor or a founder) you play in.

BTW – the process of normalization (hiring freezes 🥶, layoffs at growth companies) has already started, and some of the most respected leaders are taking the lead.